In collaboration with JENNIFER SHEN & MACKENZIE SUBEN

Money management is a fundamental skill that is particularly tricky and even intimidating to learn. The ability to understand financial choices, plan for the future, and respond to events that affect financial decisions are imperative to successful personal financial management—something which college students demonstrate poor skills in. Perhaps even more today than ever before, with tuition costs through the roof and an unprecedented amount of student debt, financial capability is key for navigating student life in order to become more financially competent.

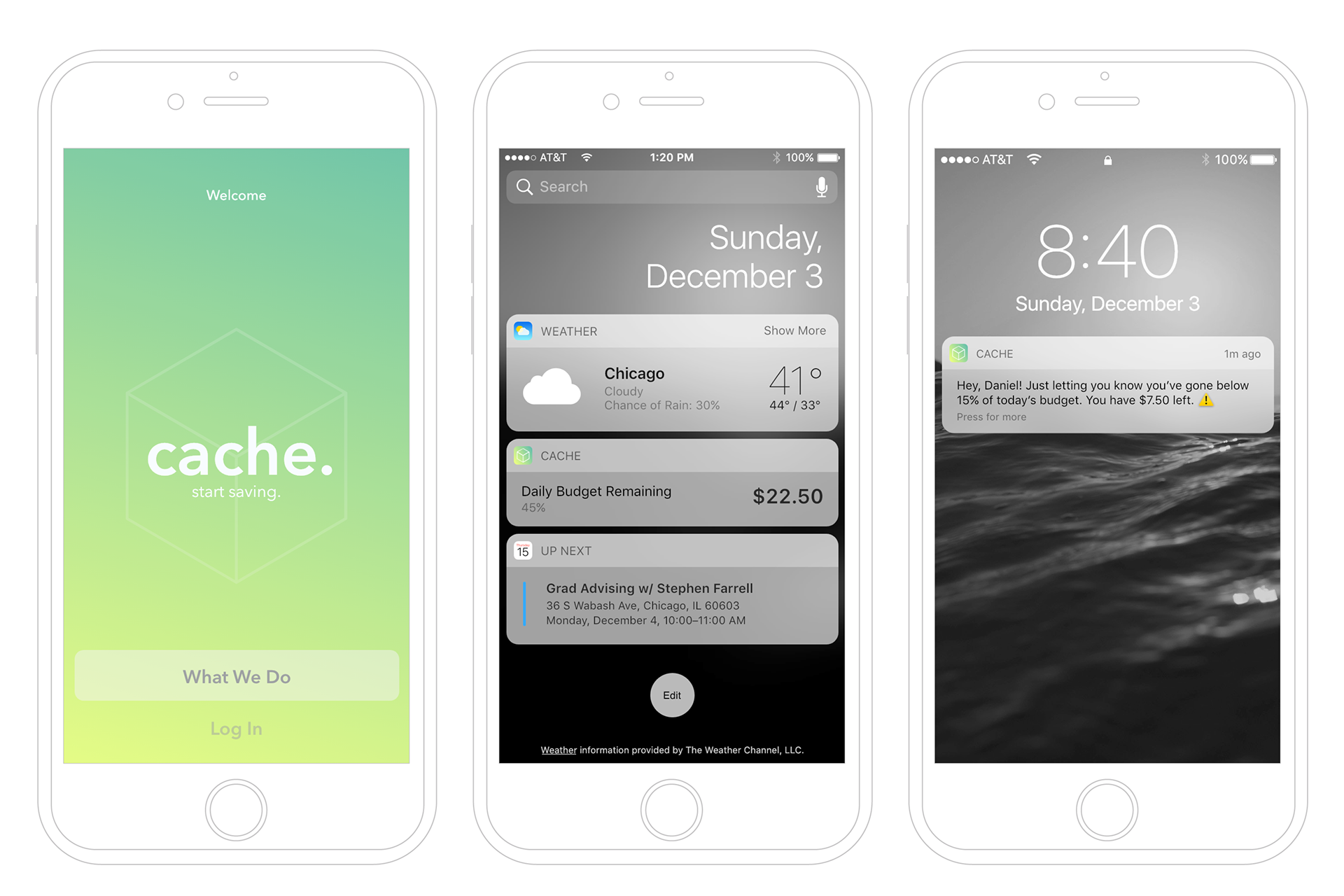

cache. is a speculative money management app concept created for an elective course that dealt with understanding and envisioning information, focusing on helping students evaluate their spending habits in a novel way and set financial goals. As part of the project brief, our team was provided a specific user profile named “Daniel” with substantial financial data.

Our approach to the app was divided into three main steps: 1) identify and analyze Daniel’s spending habits, 2) help Daniel set short- and long-term financial goals by examining his needs and wants, and 3) develop savings challenges based on habitual spending to help Daniel meet these goals. We decided to target habitual spending as these are behaviors that are easiest to curb and generate the highest reward in terms of long-term saving. The goal of the app was to use simple graphics and language, suggest healthy financial and personal habits, and implement positive reinforcement to help Daniel—and college students in general—be more financially aware and involved.

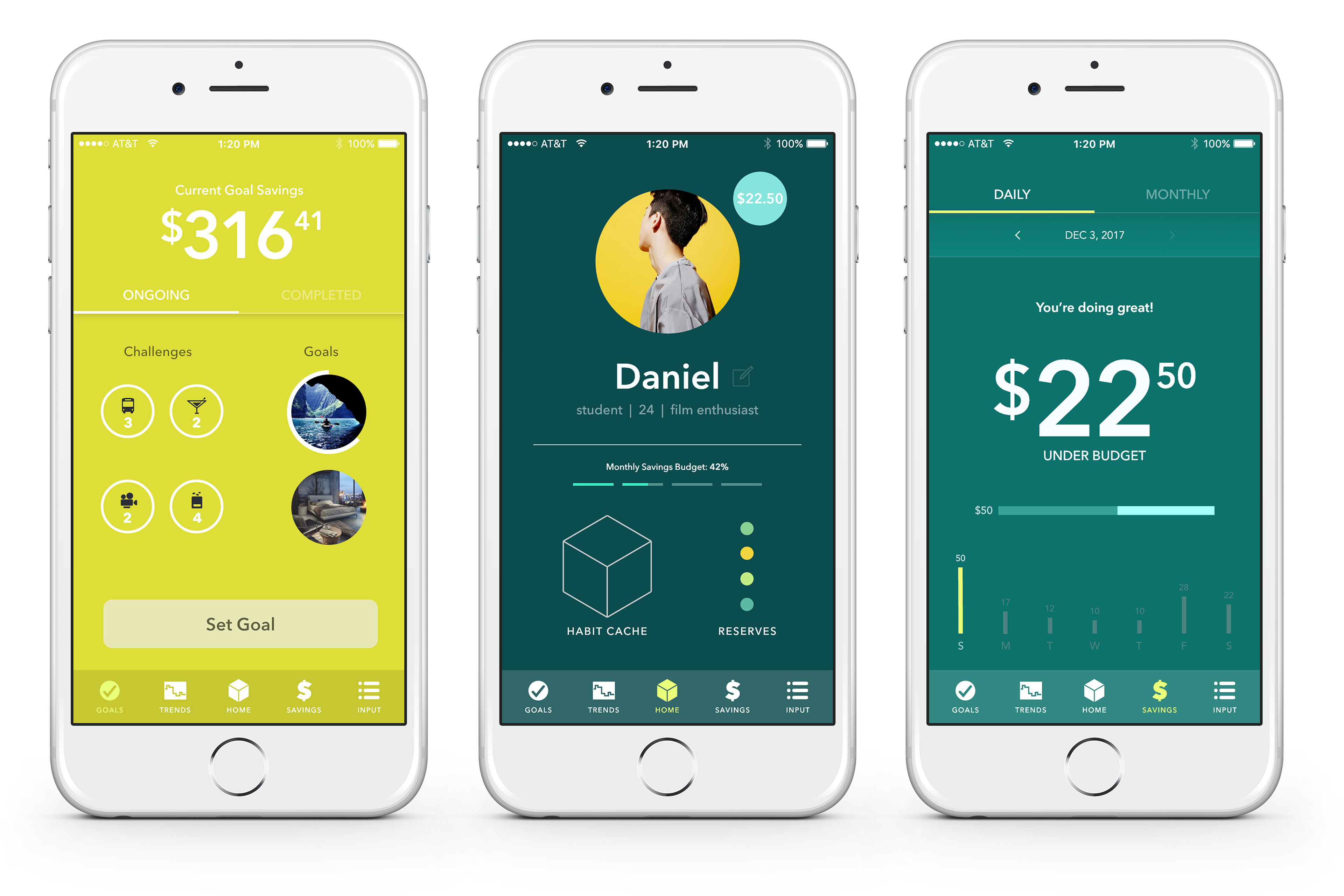

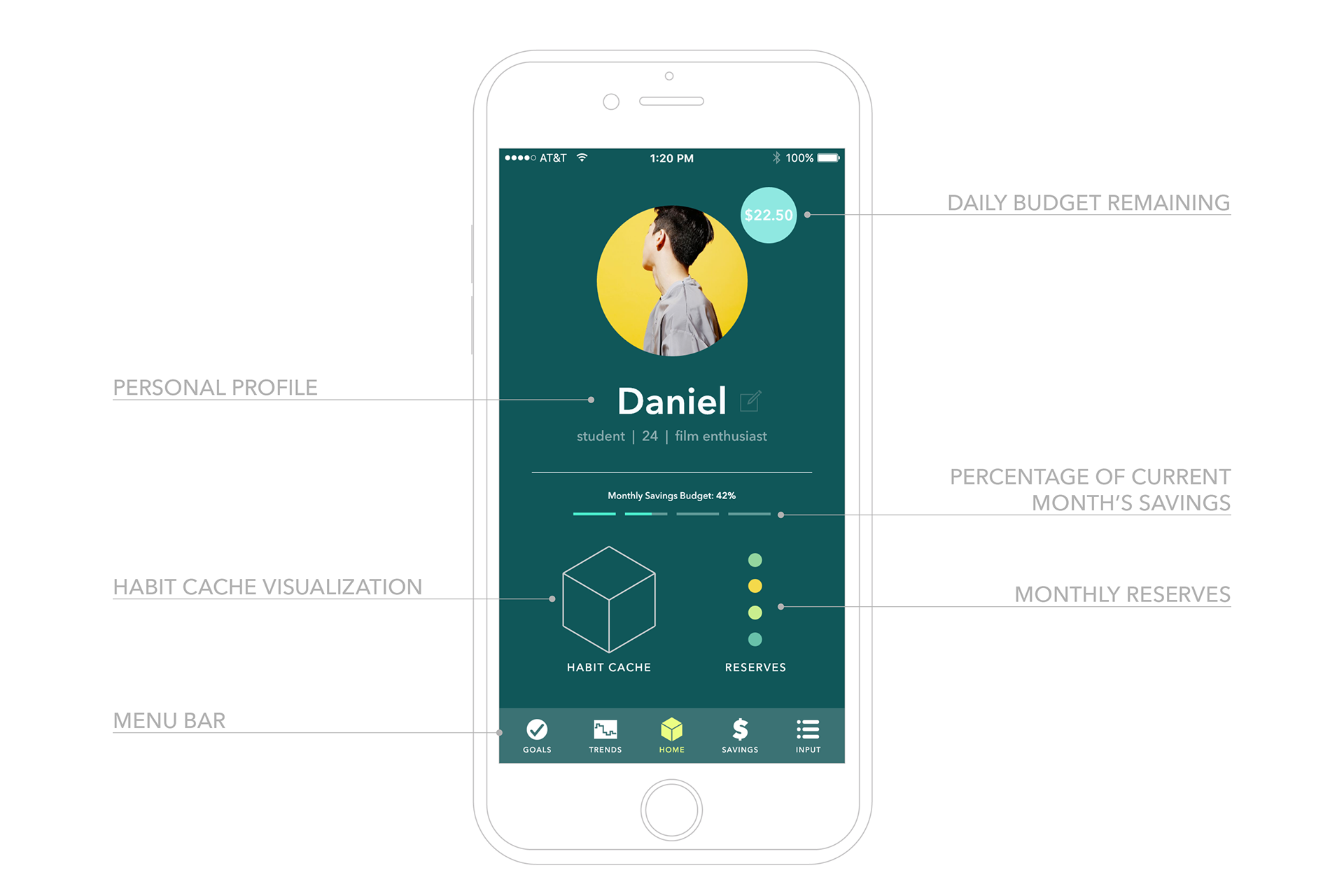

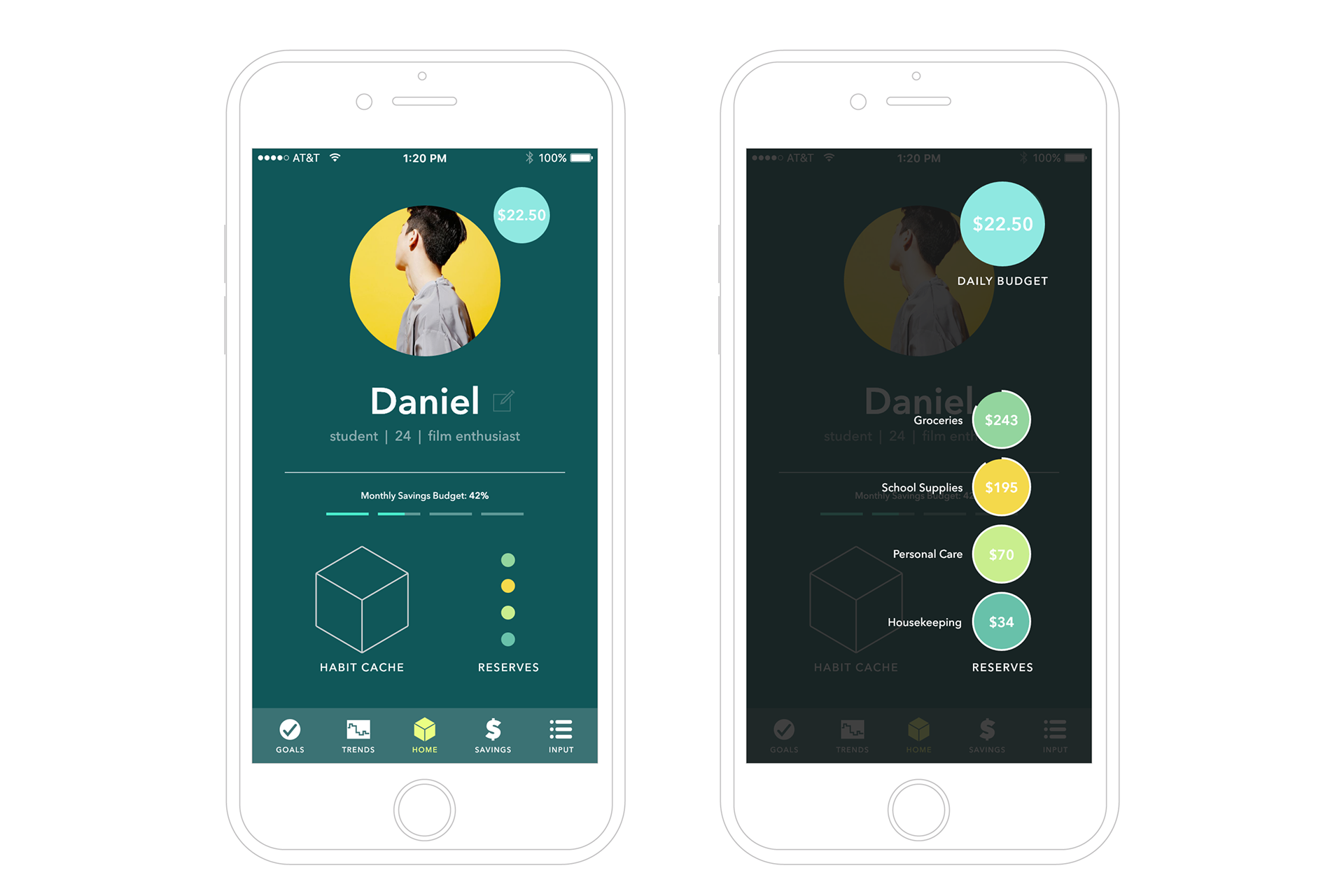

cache.’s three main features are aimed at helping Daniel understand his spending and plan accordingly. A habit cache allows Daniel to quantifiably visualize his discretionary spending within a three-dimensional matrix based on his input on individual purchases. Challenges are generated to target periodic spending that help Daniel meet his self-set goals, allowing him to be aware of his habitual spending and actively engage in saving. A fluid budget based on Daniel’s linked financial data customizes his daily spending cache to accurately reflect his lifestyle.

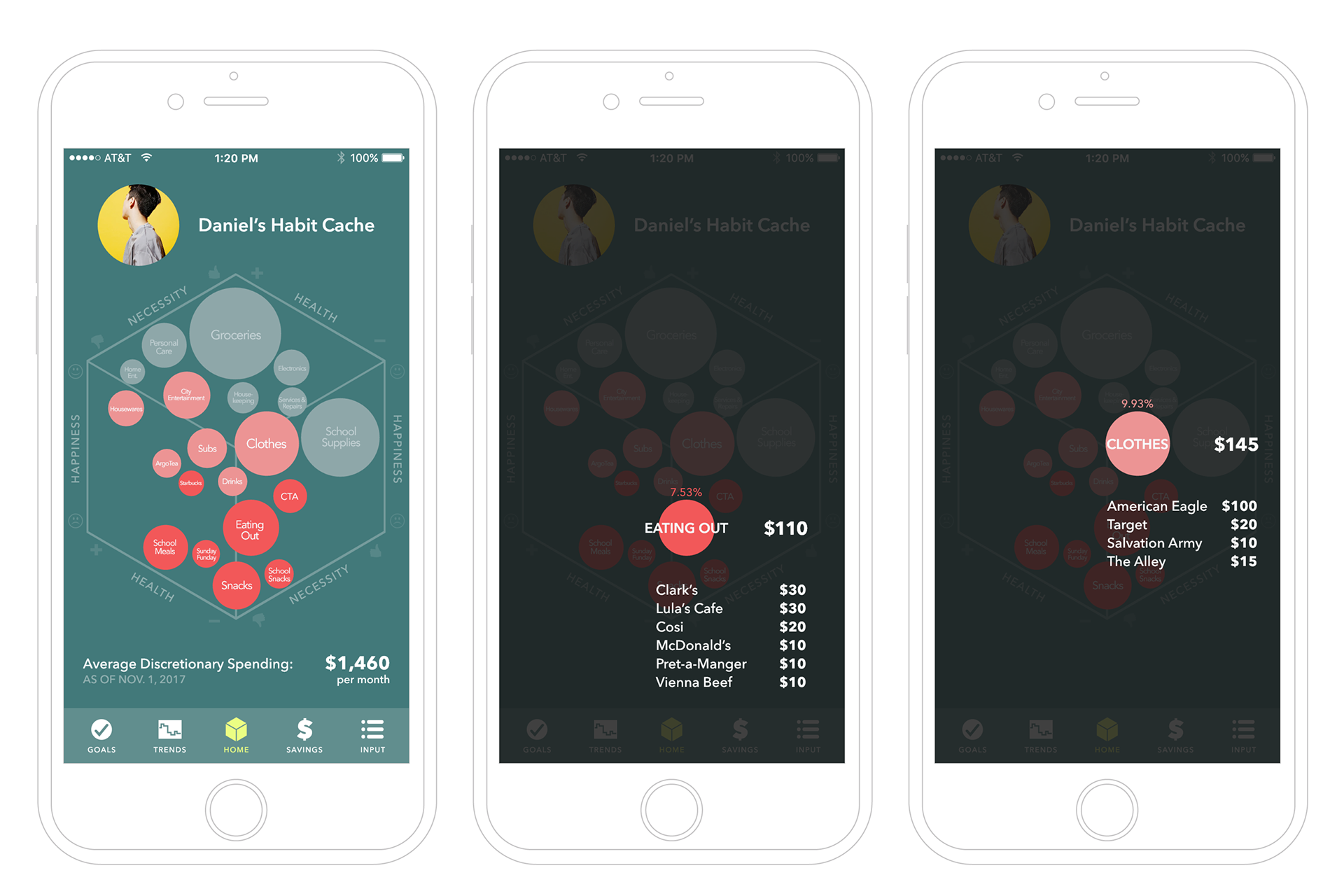

Habitual discretionary spending outputs account for a large portion of our expenses and we don’t even think about how that daily trip to Starbucks or those periodic public transit trips can affect our overall spending. The habit cache allows Daniel to visualize his expenses and understand which ones are important and which ones can be curbed, according to his own feedback. Expenses that are important are pushed back while those spending habits that could be worked on are brought to the foreground.

Many current personal finance apps, whether those provided by banks or third parties, present spending in some sort of pie chart or bar graph with broad general categories, often containing misplaced transactions. In cache., discretionary expenses are presented in smart categories that are generated from Daniel’s lifestyle according to his spending habits.

It was important to us that Daniel had to ability to see distinct categories specific to this spending in order to better understand and be aware of his financial habits. Each bubble category is sized according to their respective percentages of average discretionary spending and, when tapped, contains an itemized list of average transactional behavior. We felt it was important to represent this data as hard numbers rather than percentages so that Daniel can have a real-world understanding of his spending.

The habit cache is essentially a cube that translates his input data along a three-axis matrix according to necessity, health, and happiness. The bubbles in bright red indicate that those expenses aren’t necessary, aren’t the healthiest, and aren’t making Daniel happy, per Daniel’s input. Bubbles that fall within a mid-range of these axes are presented in a muted red tone, while bubbles containing expenses that are essential or meet Daniel’s matrix trifecta are in a translucent grey.

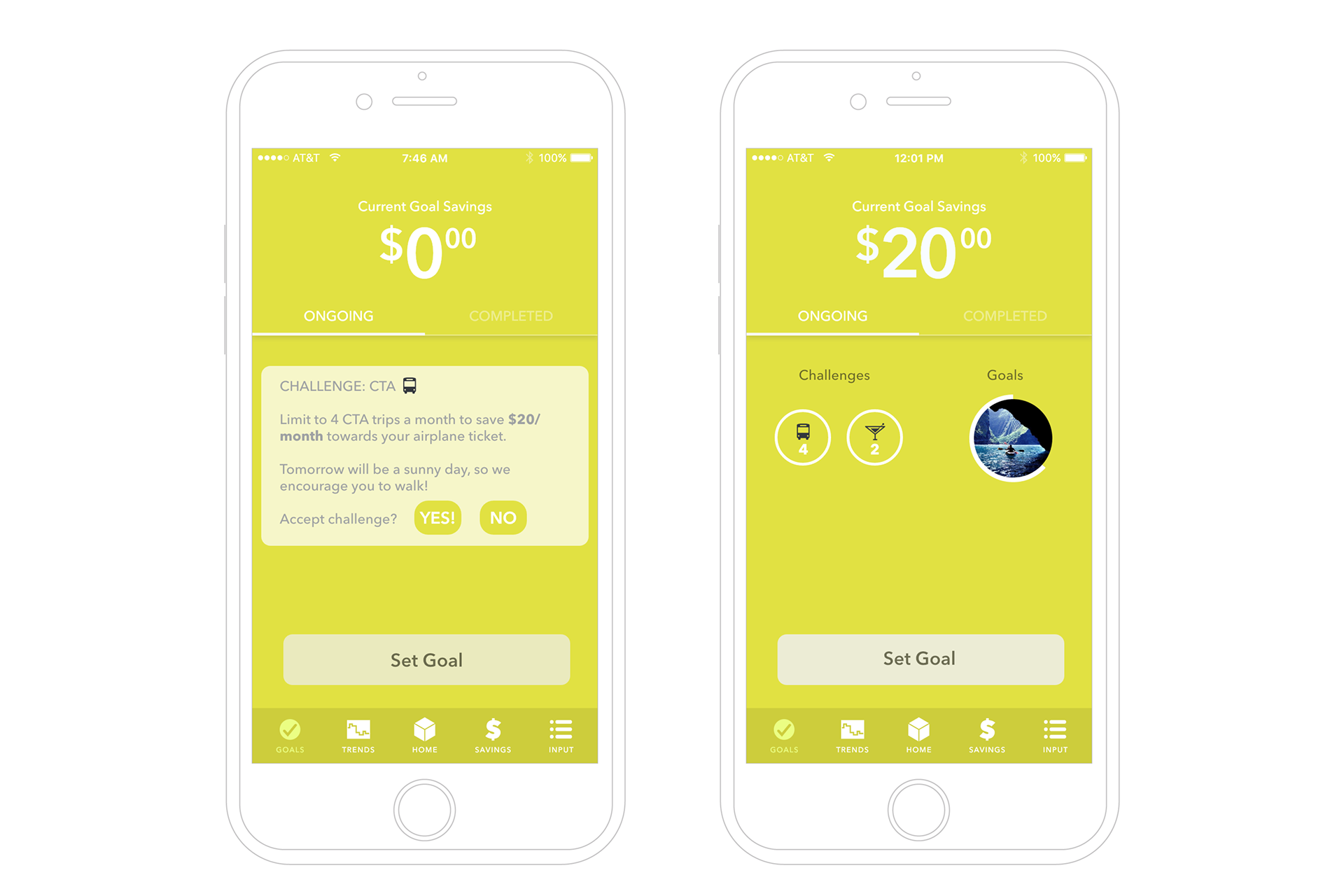

Setting goals is made easy by simply entering whatever it is that needs to be saved for, entering an amount and a date, and even the ability to upload an image for inspiration. Monthly Savings Bundles are packaged from Daniel’s purchase feedback and financial data, in turn, providing the savings Challenges to help him meet his goals. Daniel has the ability to opt out of any of the suggested habit curbs within the Savings Bundles as long as the Bundle equates to the amount needed per month to save.

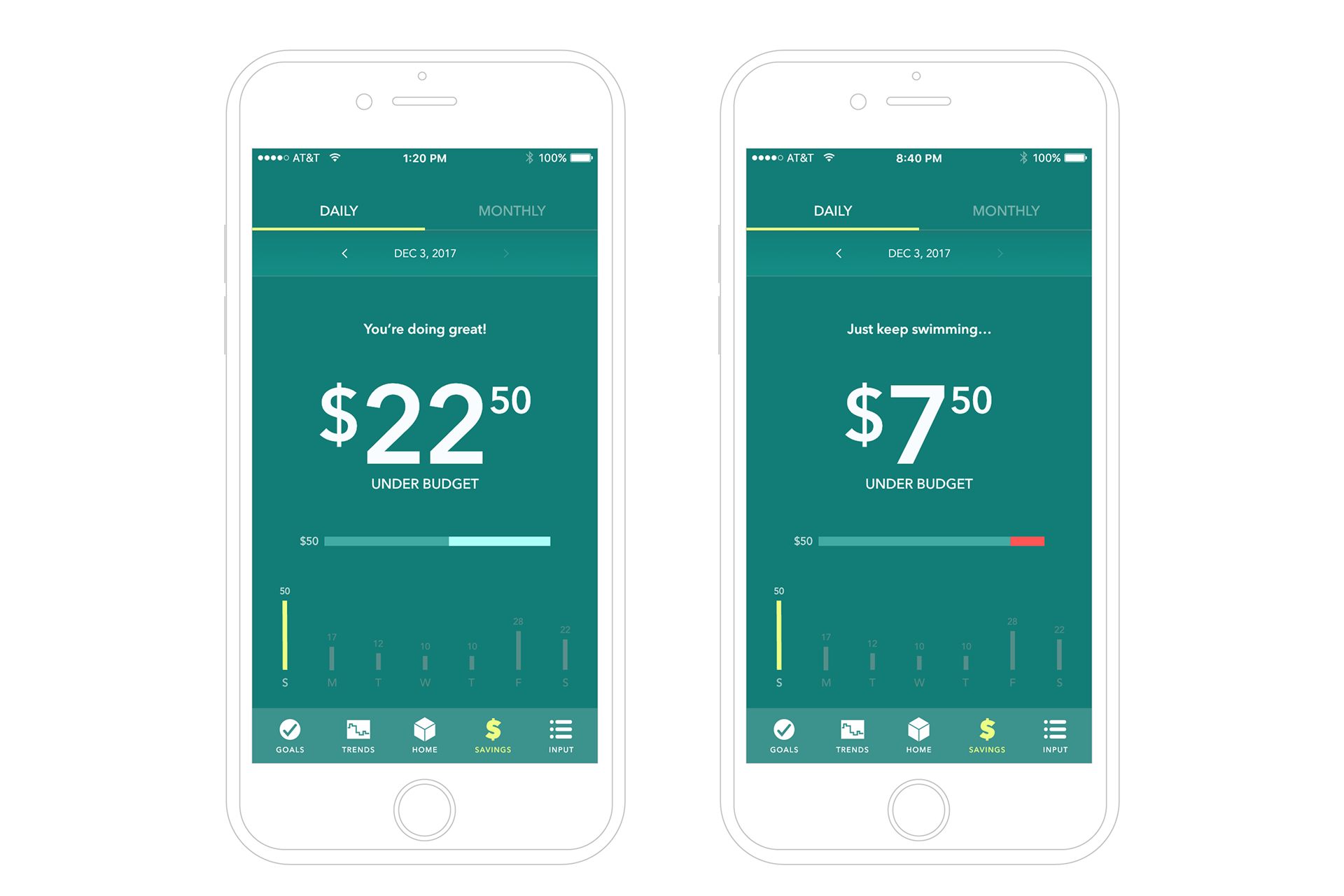

Once goals are set, Daniel receives prompts that allow him to either accept or deny Challenges. The Challenges operate on a sort of “reverse reward” system, where Daniel is given a set amount of tokens based on the particular challenge and is encouraged to only use the given amount. For example, if one of Daniel’s challenges is to cut his public transit use in half and limit his trips to four per month in order to save $20, four bus/train tokens are allotted for use. Each time Daniel makes purchases public transit fare, one of the tokens goes away. At the end of the month, his savings are calculated: the amount saved from the challenge would include the $20 from the challenge plus any leftover tokens that Daniel didn’t use that month. If he doesn’t use public transit at all that month, his savings would total $40 for the month.

Within the language of the Challenges, Daniel is given healthier alternatives to his habits such as substituting riding the train for walking or biking, or even drinking water instead that third whiskey sour. By focusing on positive reinforcement and reward systems, we limit any language that may come across as patronizing or authoritative, promoting Daniel to follow through with his savings goals. At the end of each savings period, Daniel can put all savings directly into his savings account. His Challenges are kept alongside his Goals so he can easily keep track of his progress and how many tokens he has left.

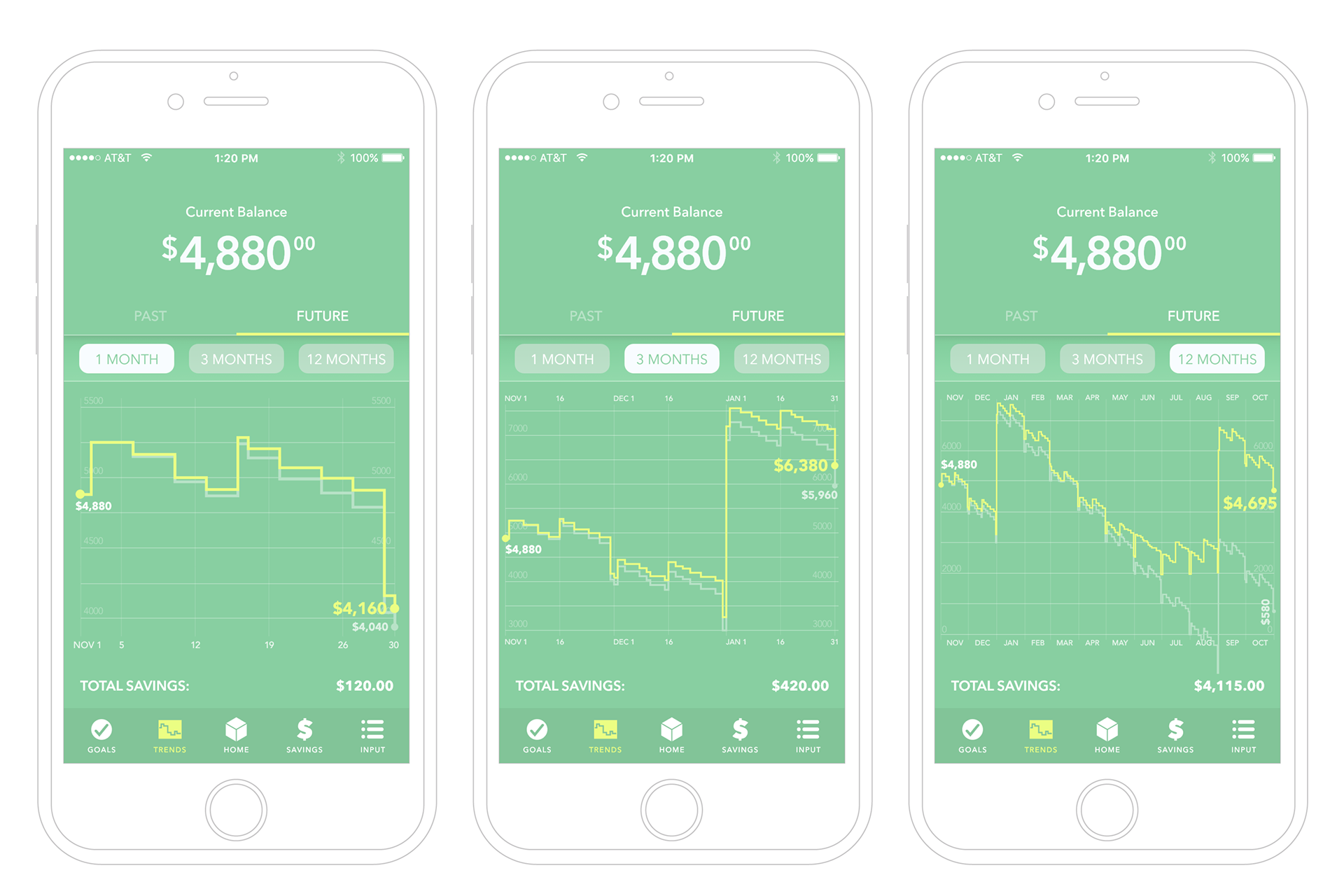

Forecasting was an essential component of the app as it is important for Daniel to be able to visualize his spending habits and their effects on his wallet in the future. Trend lines are generated to show Daniel what his bank account will look like if he continues spending the way he does versus if he sticks to the savings plans generated by his goals. The ability to forecast at various scales—one month, three months, and one year—is important in understanding spending at appropriate times in order to make informed decisions. Additionally, Daniel has the option to view trend lines for his past spending habits.

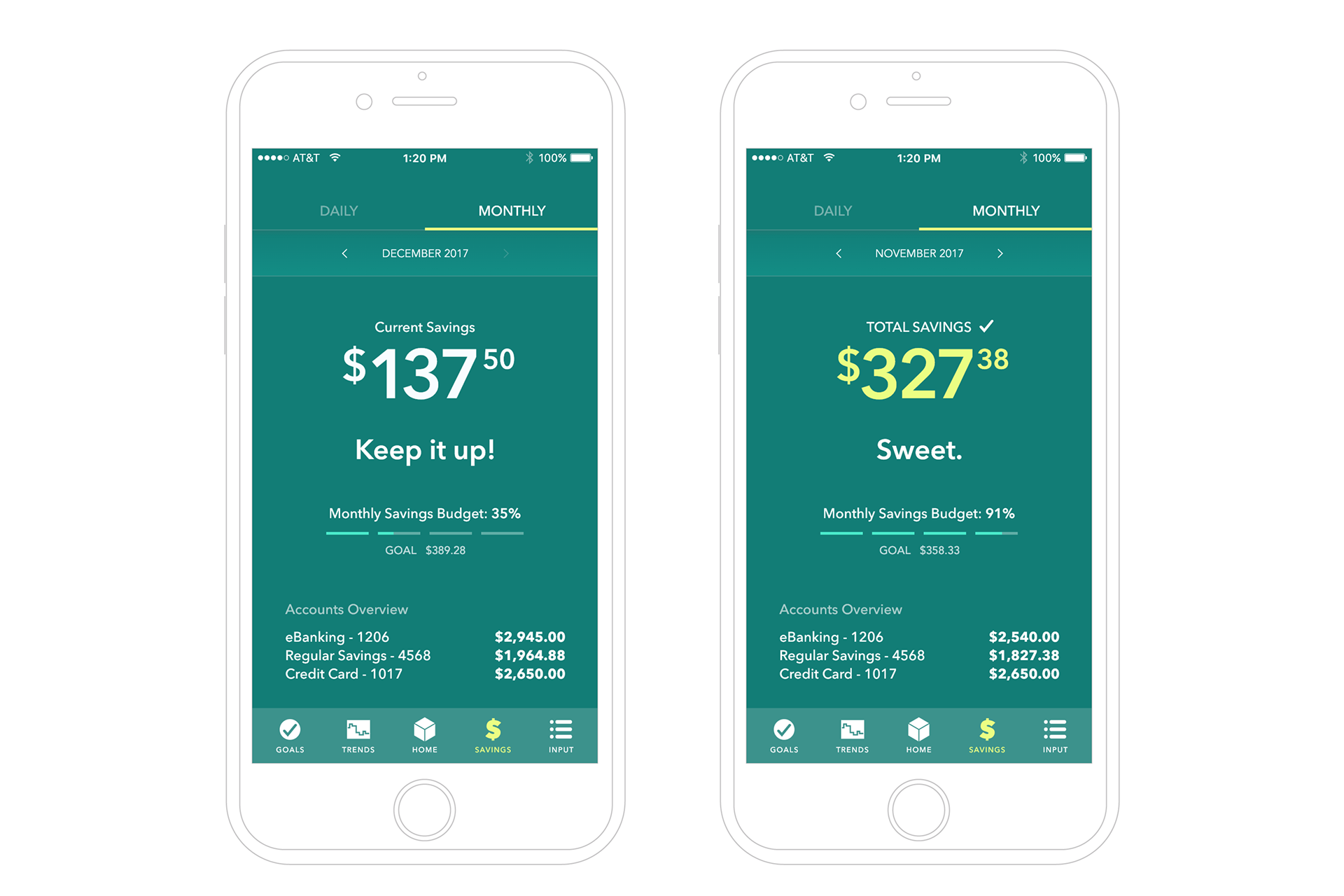

The fluidity of Daniel’s daily budget is accurately reflective of his spending needs and habits. His spending is not necessarily erratic, but isn’t constant. He tends to spend less during the week and more on weekends overall, spends more on discretionary expenses toward the end of the month, and spends more money in the months coinciding with school semesters. A fluid and flexible daily budget takes his lifestyle into account and adjusts for how Daniel spends his money. Concise monthly savings reports are available for Daniel to view and understand his progress for past months and the current month as well, allowing him to see where he’s at and where he needs to be.

Daniel is also allotted monthly Reserves for those categories of outputs that he knows he will need to spend money on such as groceries, school supplies, personal care, and housekeeping items. These are set aside and kept separate from his daily budget and are easily accessible from the home screen.

This project was a collaborative effort with Jennifer Shen and Mackenzie Suben under the instruction of Stephen Farrell at the School of the Art Institute of Chicago.

Pacheco, Shen, and Suben do not own any supplemental images pertaining to the project process or final presentation, including but not limited to: photographs of individuals or the likenesses of individuals, or additional photography. The Avenir and Avenir Next typeface families were licensed for educational use through the School of the Art Institute of Chicago.

All other images, original design elements, and combinations of elements constituting an original design are owned by Pacheco, Shen, and Suben.